Arbitrage - arises if an investor can construct a zero beta investment portfolio with a return greater than the risk-free rate

If two portfolios are mispriced, the investor could buy the low-priced portfolio and sell the high-priced portfolio

In efficient markets, profitable arbitrage opportunities will quickly disappear

*Note: we will explore more of this with derivatives later

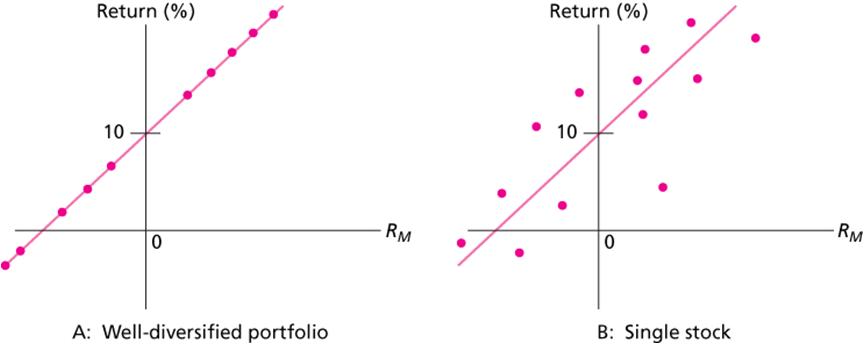

Figure 7.5 Security Line Characteristics

APT and CAPM Compared

APT applies to well diversified portfolios and not necessarily to individual stocks

With APT it is possible for some individual stocks to be mispriced - not lie on the SML

APT is more general in that it gets to an expected return and beta relationship without the assumption of the market portfolio

APT can be extended to multifactor models

No comments:

Post a Comment